‘Why has the budget deteriorated despite the windfall increase in revenue? And where has the money gone?” JON STANHOPE & KHALID AHMED return to the revenue questions in the ACT Budget.

The latest ACT budget shows an increase of $842 million in the forecast revenue from the 2025-26 forecasts over the four-year period 2025-26 to 2028-29.

Correspondingly, over the same period, the 2026-27 budget reveals an increase in expenses of $1.389 billion.

As a result, the Net Operating Balance deteriorates by $547 million over this period.

In this article, we further analyse the budget to highlight the main contributors to the increase in revenue.

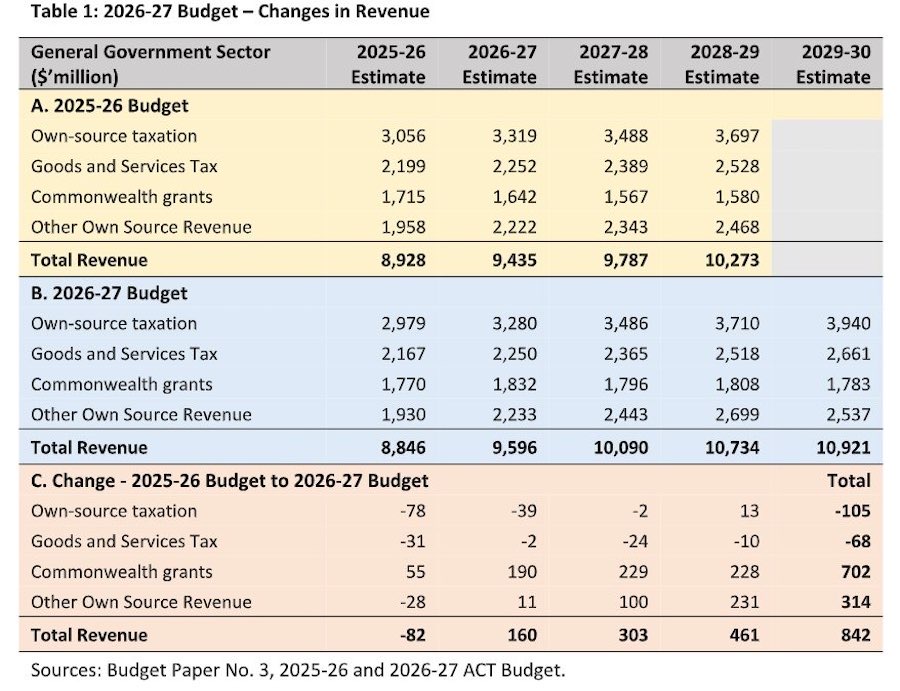

Table 1 provides the revenue forecasts in the 2025-26 budget (Table 1A), the 2026-27 budget (Table 1B), and changes in forecasts in this budget (Table 1C).

The table, and similarly, Table 1 in our previous article, highlight the changes in the base budget. The table presents total revenue disaggregated into four broad categories: own source taxation (34 per cent), GST revenue payments (25 per cent), Commonwealth grants (20 per cent), and other own-source revenue (22 per cent), with the figures in parenthesis indicating the approximate share of each category in 2025-26.

The revenue collection forecast is $82 million below budget in 2025-26 (the current financial year about to conclude). However, a significant increase across the forward years is forecast, largely driven by an increase in Commonwealth grants and continued optimism in revenue growth.

Own source taxation

There are, in the budget, 21 individual tax lines comprising taxes on payroll, dwellings, land, and transactions, as well as various levies. The decrease of $105 million shown in Table 1C is largely due to the removal of the $100 health levy from general rates and a downward adjustment ($15 million a year on average) to payroll tax, following an expected shortfall of $32 million in 2025-26.

Payroll tax is still forecast to grow at a staggering rate of 10.4 per cent. The impact of this tax is mainly on employment and the cost of goods and services for consumers, depending on market conditions. Clearly, there are downside risks – larger than the previous year – to achieving the forecast payroll tax.

While there is an apparent decrease, general rates are nevertheless budgeted to grow at 8 per cent on average. In what, one imagines, would be an embarrassment to any other government, revenue from stamp duty on residential dwellings has been boosted by $38 million compared to the 2025-26 estimates.

The ACT Government now collects about 25 per cent more from this tax than it did when it initiated the reforms designed to abolish the tax altogether!

Land tax is forecast to deliver $27.5 million more than previously forecast. This is a tax imposed on rental properties and is expected to reap $1.1 billion, in total, over the budget and forward estimates period.

Under the government’s stated policy, it should have been abolished by now or, at a minimum, the tax rates should have been reduced, noting that the ACT has the lowest rental affordability and the worst levels of rental stress in Australia.

There are remissions for the lease variation charge averaging $4 million a year (strangely, the budget papers refer to only $2.1 million a year being attributed to development incentives) with an unquantified benefit in the number of additional dwellings supplied.

The revenue forgone is offset by the Police, Fire and Emergency Service Levy (PFSEL) which is increased at 2 percentage points above the Wage Price Index (WPI) rising to 5 percentage points “peg” in 2028-29. The Safer Families Levy is escalated by $5 in each of the next three years to reach $85.

These are lazy and arbitrary increases in flat taxes that are imposed equally on both the rich and poor, the young and old – and hence regressive and without any underlying principle.

GST revenue and Commonwealth grants

GST revenue is largely unchanged, being determined by the relativity assessed by the Commonwealth Grants Commission and the size of the national pool. We have previously explained the principles of the assessment framework in our articles.

Commonwealth grants include financial assistance grants for local government, municipal services, Specific Purpose Payments (SPPs) and payments under the National Partnership Agreements (NPPs).

Over the period 2025-26 to 2028-29, Commonwealth grants provide an additional $702 million to the ACT’s revenue base.

For space considerations, we have not included a detailed breakup of the grants, however, notably $550 million of the increase relates to recurrent grants, largely for health, and $152 million in capital grants. The latter amount improves the apparent operating balance due to the accounting treatment of capital grants, but is not available for the recurrent budget.

Other own source revenue

This revenue identified in Table 1 aggregates more than 20 individual revenue lines related to regulatory fees and service charges, as well as some non-cash items such as gains from contributed assets. The increase of $314 million is largely driven by anticipated additional revenue from cross-border payments for hospital services.

In 2025-26, cross-border revenue from NSW delivers $109 million above the budgeted amount, which the budget papers advise relates to a back payment.

However, the increase is carried across the forward years thereby adding $381 million to the revenue base. Notably the 2025-26 deficit outcome would have been worse (-$916 million) but for this back payment.

The above analysis compares the revenue estimates in this budget with the previous budget over the period 2025-26 to 2028-29. The 2026-27 budget has added a new forward year, 2029-30, to the forward estimates period. The increase in the revenue base over the budget and forward estimates period (2027-28 to 2029-30) is more than $1 billion.

The combination of Commonwealth health grants and cross-border payments have delivered an additional $769 million in revenue over the estimates period.

Despite the windfall revenue from the Commonwealth and NSW, the government’s overall policy approach to raising revenue remains extractive with taxation revenue growing at a compounding annual rate of 7.2 per cent, and other own-source revenue including fees and charges growing at 7.1 per cent, both more than double the forecast economic growth rate. It is also regressive and, in some cases, without any underlying principle.

Our fellow columnist, Michael Moore has noted that profits coming from rezoning of land should belong to the people rather than the developer. The government has foregone the rezoning benefits, but is happy to compensate for that by increasing tax on renters. The budget withdraws the $100 health levy but increases another levy by $15. Those changes, apparently small and unnecessary, paint the government as petty, mean and unprincipled.

However, the two key remaining questions are:

- Why has the budget deteriorated despite the windfall increase in revenue?

- And where has the money gone?

Jon Stanhope is a former chief minister of the ACT and Dr Khalid Ahmed a former senior ACT Treasury official.

News all day, every day at CityNewsQBN.com.au.

Leave a Reply