Here’s something you might have missed: Treasurer Barr is budgeting to more than double the revenue from fines. JON STANHOPE & KHALID AHMED assume that means double the number of traffic and other cameras. But, of course, there’s more…

THE significant increase in revenue forecast in the 2023-24 budget contributes to an apparently miraculous turnaround in the ACT’s budget position.

However, the media release issued by Treasurer Andrew Barr upon release of the budget is essentially silent on the amount and source of the anticipated increase in revenue.

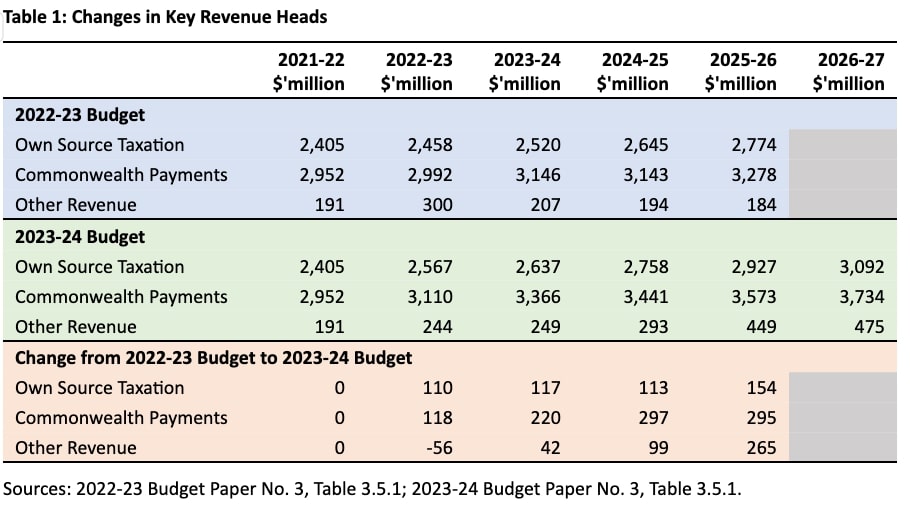

The anticipated growth in revenue can be measured by comparison with the original budget for the previous year. In this instance it reveals that about 92 per cent of the revenue increase relates to three sources – Own Source Taxation, Commonwealth payments (comprising GST and Commonwealth Grants under various agreements) and Other Revenue.

Table 1 incorporates the 2022-23 and 2023-24 budgets’ estimates and the budget-to-budget changes in these three revenue sources. The table also includes the actual outcomes for 2021-22.

Payments from the Commonwealth will deliver an additional $813 million over the three years 2023-24 to 2025-26. This largely relates to GST revenue due to an increase in the ACT’s relativity as assessed by the Grants Commission.

Averaging just under $300 million annually, this is clearly not enough to cover the operating deficit.

Treasurer Andrew Barr intends, therefore, to raise a further $789 million over the period from Own Source Taxation ($383 million) and Other Revenue ($406 million).

Taxation revenue growth in this Budget has jumped to 5.2 per cent a year from 3.6 per cent in last year’s Budget, which is well above the forecast growth rate of the economy. The budget also includes new revenue measures, not mentioned in the treasurer’s media release, nor in reporting by the mainstream media. The first hint of these new imposts is on Page 43 of Budget Paper No. 3: “This budget includes a package of carefully sequenced measures to raise revenue to meet our growing needs. This includes changes to Payroll Tax, the Fire and Emergency Services Levy, the Utilities Network Facilities Tax and the Lease Variation Charge.”

For additional information one is referred to the quaintly titled Chapter 3.2: “Investing in the Wellbeing of Canberrans”. There appears, unfortunately, to be no separate section on new revenue measures, rather, they are strewn across the more than 140 pages of this chapter. Notably these “carefully sequenced” measures kick in after the next ACT election, and their timing is purportedly premised on cost-of-living pressures easing by that time.

The Fire and Emergency Services Levy has been renamed the Police, Fire and Emergency Services Levy (PFSEL), and is increased by 4.3 percentage points above the Wage Price Index (WPI), a departure from long standing policy to index taxation by WPI. The increase will deliver an additional $12.9 million over the last two forward years.

Budget introduces a payroll tax surcharge

The Budget also introduces a payroll tax surcharge for large businesses from 2025-26 at the rates of an additional 0.25 per cent and 0.5 per cent on ACT wages above the payroll tax threshold for businesses with Australia-wide wages above $50 million and $100 million respectively. This measure, along with “increased compliance”, that is, presumably, from medical practices, will raise an additional $71.2 million over four years.

The rate of the Utility Network Facilities Tax (UNFT) will also increase by 2.5 per cent above the WPI, again, a departure from long standing policy, delivering an additional $4.9 million over four years. Changes to the Lease Variation Charge schedules, which have remained unchanged since 2017, will deliver $22.4 million over four years.

However, the government’s professed concern about cost-of-living pressures have not been reflected in its decision making.

Land tax (imposed on rental dwellings), which the government promised, a decade ago, to abolish, under its tax reform program, is forecast to increase by 13.3 per cent in 2023-24, delivering an additional $25.4 million.

The proposed increase in the Lifetime Care Levy, and PFESL will also directly impact households, while the increase in the rate of UNFT will assuredly be accounted for in future price determinations for utilities.

Businesses, in particular, face uncertain costs, likely to be revealed after the next election, with respect to PFESL as the budget papers do not provide any indication of the marginal tax rates applicable to commercial properties once the increase is instituted.

The increase in the Fire and Emergency Services Levy is in effect a new tax rather than an increase in the rate of an existing tax. The genesis of the levy was to replace a tax on insurance policies for emergency response through a charge on general rates.

However, the government is now seeking to recover costs of policing services through this base – a service that has always been funded from general revenue.

Revenue measures ‘opportunistic and incoherent’

In relation to payroll tax, it is erroneous to assert that the surcharge will have no effect on households. The economic incidence of this tax is, depending on the circumstances of the economy, on consumption (ie, household budgets) or employment.

The revenue source “Other Revenue” rakes in $406 million over three years from a base of just $191 million in 2021-22, increasing at a compounding annual rate of 20 per cent. Within this aggregate, fines are forecast to more than double from $48.8 million in 2022-23 to $104.1 million in 2025-26.

While no explanation has been provided for such a dramatic increase in fines, one assumes it will involve a doubling in the number of traffic and other cameras and/or a dramatic increase in speed vans.

There is extraordinary opacity about several other revenue items under this source, for example, Big Canberra Battery ($47 million over two years) and increase in Other Grants reaching $188 million from a base of a mere $5 million in 2021-22.

In summary, the revenue measures in the budget are both opportunistic and incoherent, and not reflective of a fair and efficient tax system.

In addition to justifiable concern about the social and economic impacts of the new revenue measures, there is, considering Treasurer Barr’s unmatched Australian record of 12 consecutive budget deficits, a massive question mark over whether the forecast improvement in the operating budget will eventuate.

Jon Stanhope is a former chief minister of the ACT and Dr Khalid Ahmed a former senior ACT Treasury official.

News all day, every day at CityNewsQBN.com.au.

Leave a Reply